Back in the 1970s, when Uncle Joe told me this joke, it was a comment on how automation was going to replace humans — an acknowledgment that humans can make costly errors by pressing the wrong buttons, in the wrong order, or at the wrong time. But through the years, I have been reminded of this old joke many times over, as it speaks to much broader themes about the human condition. I thought about it during my Eastern Religion & Philosophy undergraduate classes where we read Taoist teachings of wu wei (which advocates finding enlightenment by not obsessing, not thinking or trying too hard, but rather through “doing by not doing,” the literal translation). The theme appeared in pop culture, with the Lennon-McCartney lyrics and Mother Mary telling us what to do in times of trouble or our hour of darkness – let it be, let it be.

As it relates to my chosen profession of finance and investment management, I thought about it during my MBA days reading Adam Smith’s Wealth of Nations or essays by Milton Friedman who both espoused laissez faire (let it be) economics; it told us humans to take a hands-off approach to regulations and controls, and instead, let the invisible hand of markets do their thing. And any behavioral finance article you pick up today will have eye-opening data proving why we flawed humans – suffering from a veritable laundry list of biases — should resist action bias (the burning desire to “do something”), recency bias (what is happening now is likely to continue), and overconfidence bias (thinking, “I am very skilled at something”, despite evidence to the contrary), to name a few.

But more importantly, I am thinking about Uncle Joe’s joke this week, as we all experience uncomfortable drops in stock market prices. There arises this primordial urge to grab the cockpit controls and “do something.” And we must remind ourselves that despite all experience and literature from the ages about the folly of trying to time markets, we still want to do it. We remain confident in our abilities despite mountains of evidence to the contrary. These are very human and very common impulses…that we must resist.

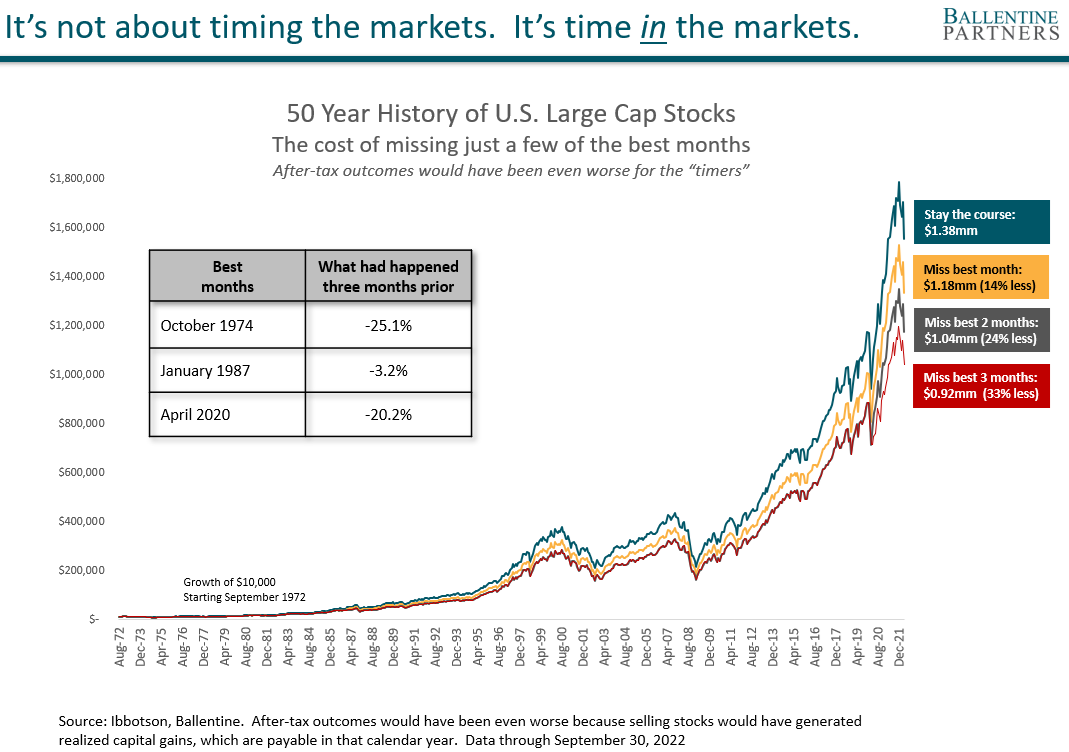

We must resist them because the stock market is a fickle and moody beast. While its movements can always be explained after the fact (our brains are literally hard-wired to love a linear narrative that makes sense), the reality is a bit more messy. Good news is bad news some days. And bad news is good news other days. So trying to time these moves is not just folly but extremely costly. Which brings us to the chart below. I will state up front that the following analysis is by no means unique or new. I joined the investment management industry in the 1980s, and thoughtful advisors have been publishing different flavors of it for years. Still, it is worth dusting off today. The message is simple. The best way to compound wealth in the stock market is not about timing the markets. It is about time in the markets.

What you’re looking at below is a chart showing the growth of $10,000 invested in US large cap stocks over the last 50 years. If you had simply left the money alone, i.e., stayed the course, that initial investment would have grown to $1.38 million, a tidy sum. This is the power of time, the power of compounding, and frankly, the power of “letting it be.” If instead, investors had started tinkering, thinking they had some sort of timing model, they started playing a perilous game – perilous because the stock market can move in dramatic fashion, short bursts, so to speak. And if an investor happens to miss one of those short upward bursts by being in cash, the economic impact can be devastating. See below. If an investor had just happened to miss the best single month, their wealth would have dropped significantly, a 14% haircut. If they had missed the best two months, that $1.38 million would have dropped by a quarter. And if they had missed the best 3 months, their wealth dropped by 33%. In other words, you could have had a batting average of .995…and still have your wealth cut by a third!

“Yeah, but you cherry-picked the best three months. What are the odds of that?” might be your counter-argument. And that would be a reasonable push-back. But is it, really? It turns out that many of these very good months happened right after a massive, gut-wrenching drawdown, the exact moment when our primordial urge to do something would have kicked in. So, in fairness, it is not a far-fetched analysis, at all.

We want to be clear. We are NOT suggesting that you do absolutely nothing. There are actually a plethora of things we are recommending to our clients right now. There are sizable tax-loss harvesting opportunities for any cash that was put to work in the past six to nine months. For those who had not started or had suspended any dollar-cost averaging programs, now is the time to consider re-starting or even accelerating it. Certainly, we are suggesting a rebalance to strategic weights. On the bond side, the run-up in rates has left bond pricing, particularly on the longer end of the curve for Municipals at attractive levels (at a time when municipal finances are in extremely good shape). While we are still having a spirited debate internally on this topic, the run-up of the U.S. dollar has left the Euro the cheapest it’s been in over 20 years (leaving European exporters with a huge pricing advantage and which historically has led to a nice pop in earnings for European companies). And much more. I think you get the point. There is plenty to do.

But we understand. It’s not fun to live through this kind of volatility. But this is the price to pay for the dramatic wealth-building capability of equities. Equities are awe-some in the long term, not despite, but because they can be so aw-ful in the short term. In this seeming hour of darkness, however, the key is to let it be.

About Pete Chiappinelli, CFA, CAIA, Deputy Chief Investment Officer

Pete is Deputy Chief Investment Officer at the firm. He is focused primarily on Asset Allocation in setting strategic direction for client portfolios.

This report is the confidential work product of Ballentine Partners. Unauthorized distribution of this material is strictly prohibited. The information in this report is deemed to be reliable. Some of the conclusions in this report are intended to be generalizations. The specific circumstances of an individual’s situation may require advice that is different from that reflected in this report. Furthermore, the advice reflected in this report is based on our opinion, and our opinion may change as new information becomes available. Nothing in this presentation should be construed as an offer to sell or a solicitation of an offer to buy any securities. You should read the prospectus or offering memo before making any investment. You are solely responsible for any decision to invest in a private offering. The investment recommendations contained in this document may not prove to be profitable, and the actual performance of any investment may not be as favorable as the expectations that are expressed in this document. There is no guarantee that the past performance of any investment will continue in the future.