The Christmas season is in full swing, with decorations for sale at Home Depot and adorable family photo cards starting to show up in our mailboxes. It’s also time for the continual loop across cable channels of Frank Capra’s classic holiday movie, It’s a Wonderful Life, starring Jimmy Stewart. The movie has so many life-affirming messages that I feel a little guilty tying it to anything money-oriented. But here it goes.

The plot, as you recall, revolves around George Bailey, a small-town do-gooder with big ideas and big aspirations. In almost all aspects of his longing – college, a career in architecture, global travel, love — George wants a big life away from quaint, but stultifying, little old Bedford Falls.

There’s the scene above where George tells his father that he doesn’t want to work at a piddly family-owned Bailey Savings and Loan bank, that he’s got much bigger plans. Later, we hear:

I’m shaking the dust of this crummy little town off my feet, and I’m gonna see the world. Italy. Greece. The Parthenon. The Coliseum. And then I’m gonna build things. I’m gonna build airfields. I’m gonna build skyscrapers a hundred stories tall. I’m gonna build bridges a mile long.

Then there’s the scene where George proudly boasts about their larger-than-life honeymoon plans:

You know what we’re going to do? We’re going to shoot the works. A whole week in New York. A whole week in Bermuda. The highest hotels, the oldest champagne, the richest caviar, the hottest music…

Yet, at every turn, fate throws George a cruel curveball. The death of George’s father compels him to give up his dreams of college and a grand career in architecture in order to run the bank. He gives up the dream of traveling to Venezuela and the Yukon to spare his brother from having to run the Savings and Loan. And a run on the bank ruins Mary and George’s grand honeymoon plans.

George’s resentment towards his pedestrian life simmers over the years imperceptibly, but it erupts one fateful day when Uncle Billy accidentally loses the bank’s deposits. The bank teeters on the brink of ruin. Desperate, he’s reduced to asking his arch-nemesis, Mr. Potter, for help. But Potter chides him, “You’re worth more dead than alive.” And George, looking back on all of his seemingly small possessions and all his unfulfilled grand plans and ideas, believes him. So he contemplates suicide.

It is only through the divine intervention of a lovable yet bumbling guardian angel, Clarence, and a clever trick — George sees what life would have been had he never been born — that George is taught a very different lesson. That all the little stuff in life — the drafty old house, the old Bailey Savings and Loan, the quaint little town of Bedford Falls, the love of family and friends, and of course, ZuZu’s petals — are what really had made his life so wonderful, not the big stuff. And by those measures, George is, as his brother Billy’s toast at the end of the movie rightly claims, “the richest man in town.”

Thanks for indulging me as I tell you about a movie that you’ve already seen a dozen or more times. But the other day, I was staring at some investment data, and it got me thinking about George and ZuZu’s petals.

It was a simple analysis but powerful, nonetheless. It was a look at how an investment strategy that we have used frequently here at Ballentine Partners for many years has performed. It is a low-cost ETF (exchange traded fund) that is unmanaged. It gives investors simple exposure to small cap stocks here in the U.S. It has kind of a bad reputation, though. Unimaginative. Humdrum. Average. Unexciting. Many of our clients, spoken or unspoken, might even wonder, “Why am I paying you to find me that boring old thing? I want a BIG idea!”

We think it has this reputation because there exists a belief and narrative in the investment industry that small cap is where active managers should be able to add the most value. Surely this must be the case, the argument goes, because of the following beliefs:

- That small cap names are misunderstood

- That small cap stocks often have a very few analysts covering them, so the space is chock full of inefficiently priced names

- That small cap names are often “diamonds in the rough” — that is, a particular industry might not be attractive, but a hard-working, quick-thinking young analyst can discover that big idea

- The small cap names often are in the most dynamic parts of the economy — unproven areas with high risk and high reward profiles, so any sharp analyst can unearth these new innovative and disruptive companies

In other words, there is a lot of excitement and hope in small cap. And a belief that a smart, ambitious analyst can deliver big excess returns. Think young George Bailey: full of big ideas, eager to make his mark on the world, with aspirations of being on the cover of Barron’s as the next wunderkind stock picker, willing to make big bets and unquestioningly confident in their abilities. Surely a concentrated collection of these big ideas must be able to beat a broad, unmanaged, naïve, unthinking portfolio with no skill or judgment applied whatsoever. It’s almost an unfair fight, or so the thinking goes.

The data tells a very different story.

The reason we like this ETF is that it does not rely upon the ability of these supposed smart, “big idea” overly confident analysts who trade frequently and who charge outrageously high fees for their efforts.

Instead, it focuses on the small stuff. The stuff that really matters, as it turns out.

It has an extremely low expense ratio of only 6 basis points (0.06%). It rarely trades, so it does not incur many transaction costs nor capital gains that get taxed. It has no management fee, per se, because it is unmanaged — no team of expensive analysts, traders, or portfolio managers making buy and sell decisions. It operates as an ETF (exchange-traded fund) structure, which has some very attractive features to it as it relates to the treatment of long-term and short-term capital gains (there are none, essentially), and small cap stocks don’t generate much in terms of taxable dividends. While all these things may not seem like big exciting “impress your friends at cocktail party” investment ideas, over the long term, it’s these very features that make it so good.

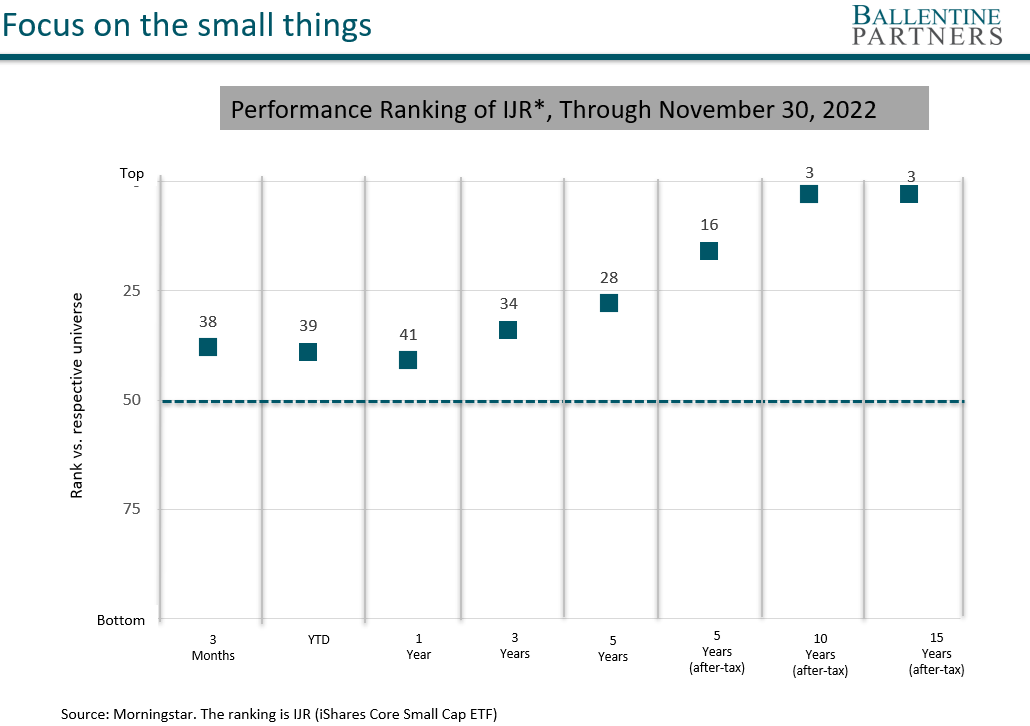

How good? Take a look. What you’re looking at below is a chart ranking the performance of our humble small cap ETF (symbol IJR*) vs. all the other active funds in the small cap category. It competes against over 620 funds in this arena, each one of them vying for excess returns. Each data plot shows how IJR ranks vs. its competition in different time frames. A rank of 1 would be the very best, 50 (the dotted line) is exactly average, and 100 the very worst. For short time horizons, IJR is a solid performer. Its three-month rank, for example, is 38th percentile. The Year-To-Date and one-year rank (through November 30, 2022) is 39th and 41st. Quite good. It improves to 34th percentile when we go out three years. By year five, though, the rank is 28th, essentially a top-quartile investment!

But it gets better. All those rankings were before any taxes were deducted. When we look at the rankings of IJR, in year 5 after-tax, the rank improves from 28th to 16th (i.e., it beat 84% of competing funds). By year 10, the rank improves to 3rd (it beat 97% of competing funds). And by year 15, its rank is 3rd (beating 97% of all competing funds).

During this entire time frame, it never relied upon an ambitious and smart team of analysts or portfolio managers to come up with big ideas. It stuck to a simple and effective strategy of doing lots of little things right. If you had owned this small cap fund over the last 15 years, compared to the entire universe of other small cap managers — many of whom have graced the cover of Barron’s and been interviewed on CNBC, true stock-picking rock stars with compelling tales of finding those diamonds in the rough — you would have been the “richest person in town”. A toast to you!

Is there no room for big ideas in a portfolio? That’s not what we’re saying. We believe quite profoundly that in other narrower pockets of the capital markets — most notably private equity, private real estate, and private credit — information is so hard to come by, the reporting so non-standard, and the idiosyncrasies of each deal so impactful that ambitious, clever, and thoughtful analytical teams absolutely can find market-beating opportunities. Our commentary above deals only with U.S. public markets where the sheer flow and transparency of information, combined with hundreds if not thousands of smart analysts competing for an edge, make simple market exposure so challenging to beat. But that’s only part of the story. There is a veritable Santa’s sleigh full of other structural factors that make big idea “alpha” so difficult to find in the public markets, but that’s a discussion for another day.

Until then, happy holidays.

About Pete Chiappinelli, CFA, CAIA, Deputy Chief Investment Officer

Pete is Deputy Chief Investment Officer at the firm. He is focused primarily on Asset Allocation in setting strategic direction for client portfolios.

*IJR is the iShares Core S&P Small-Cap ETF. The returns shown are entirely hypothetical, in that we assume an investor simultaneously made lump sum investments in an Exchange Traded Fund (ETF) and the Morningstar actively managed mutual fund universe on exactly the same date, held those investments for the entire period and reinvested all dividends. The ETF we have selected is an investable security. However, the Morningstar actively managed mutual fund universe is not an investable security; rather, it is a database created by Morningstar to track the performance of actively managed mutual funds. The results shown here are actual results, not back-tested results. All data is provided by Morningstar. The ETF we selected for this presentation represents the major market index and, in our opinion, represents an actual investment a knowledgeable investor might consider as an alternative to selecting one of the actively managed mutual funds that, according to Morningstar, invests in stocks similar to those held by the corresponding ETF. The ETF shown here is among those we consider for use in our clients’ portfolios; but, due to differing circumstances some clients’ portfolios may hold ETFs or index funds different from the one shown here. This chart is solely for educational purposes. We make no representation that any client of Ballentine Partners received the investment results shown.

This report is the confidential work product of Ballentine Partners. Unauthorized distribution of this material is strictly prohibited. The information in this report is deemed to be reliable but has not been independently verified. Some of the conclusions in this report are intended to be generalizations. The specific circumstances of an individual’s situation may require advice that is different from that reflected in this report. Furthermore, the advice reflected in this report is based on our opinion, and our opinion may change as new information becomes available. Nothing in this presentation should be construed as an offer to sell or a solicitation of an offer to buy any securities. You should read the prospectus or offering memo before making any investment. You are solely responsible for any decision to invest in a private offering. The investment recommendations contained in this document may not prove to be profitable, and the actual performance of any investment may not be as favorable as the expectations that are expressed in this document. There is no guarantee that the past performance of any investment will continue in the future.