As we age, does it make sense to structure our financial affairs before our mental capacity declines to reduce the risk of expensive financial mistakes later in life?

Summary

This article describes why it is advisable to get the right arrangements in place to protect ourselves from ourselves well before the actual need for that arises. Traditional measures such as a Durable Power of Attorney for financial management and funding a revocable living trust are not effective solutions. A self-settled irrevocable asset protection trust can be a much more effective solution.

Consider these short stories:

A wealthy elderly gentleman in the early stages of dementia paid a contractor $500,000 to “rewire” the family’s five bedroom vacation home. The contractor claimed all the electrical wiring in the house needed to be replaced, and he claimed he did so. When family members learned of this, they had another contractor inspect the house. There was no evidence any wiring had been replaced, nor was there any need to do so.

A wealthy elderly gentleman suffering from dementia was befriended by a much younger woman. He became infatuated with her and lavished expensive gifts on her. After receiving several million dollars of jewelry, clothing and other gifts, she broke off the relationship and disappeared.

Over the course of several years, a wealthy woman in the early stages of dementia transferred millions of dollars of cash to an organization in eastern Europe. When family members inquired about these transfers, she stated she was sending money to “a friend who is investing it for me.” She resisted providing additional details. Eventually, her advisers were able to gather enough information about the recipient of the funds to determine the recipient was most likely a criminal organization that specialized in exploiting elderly people.

These situations all involve a decline in mental capacity that impacted the wealth owner’s financial decision-making and resulted in significant loss of assets. We believe these types of situations will become increasingly common. Medical science seems to be able to keep us alive longer, but our brains may nevertheless succumb to the aging process. We may actually live for a long time with much reduced mental capacity.

Traditional solutions fail

The traditional solutions for managing assets during an individual’s mental incapacity include a Durable Power of Attorney and funding a revocable trust that includes provisions for a back-up trustee if the wealth owner becomes incapacitated. Unfortunately, neither really addresses the problem.

The legal system sets a very, very low bar for mental competence. An individual can be incapable of making sound financial decisions in a complex wealth situation and still be declared legally competent to manage his or her financial affairs. Furthermore, family members who are best positioned to know of someone’s declining mental capacity are likely to be subject to a conflict of interest because they may be the beneficiaries of the wealth that is being mismanaged or misdirected. A judge may question the motives of those family members if they seek to deprive the wealth owner of control over his or her assets. Besides, who wants to litigate these matters? Family members are very reluctant to go to Probate Court and seek to have Dad or Mom declared incompetent. Even if they do go to court, the chances of their prevailing are poor because of the low legal standard for competence. No one wins in litigation.

How can we protect ourselves from ourselves?

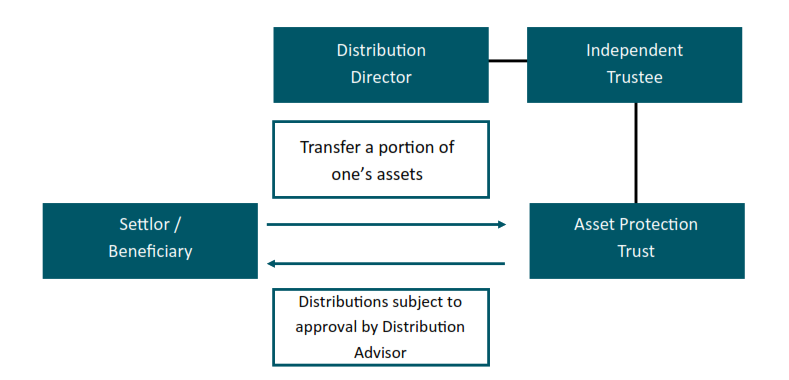

A self-settled irrevocable asset protect trust (“APT”) may offer an effective solution. Chart 1 shows the structure of a typical APT. The settlor (wealth owner) establishes an irrevocable trust in a state with laws favorable for self-settled asset protection trusts. Seventeen states offer favorable laws.

Chart 1: Self-Settled Irrevocable Asset Protection Trust

Wealth owners use APTs to protect a portion of their wealth from claims of creditors during lifetime. Because the settlor is also the lifetime beneficiary of the APT, assets held by the APT remain within the wealth owner’s taxable estate. An APT is not an estate planning trust in the sense of removing assets from the wealth owner’s taxable estate.

An APT can be used by a wealth owner to protect a portion of his or her assets from poor decision-making by the wealth owner. An APT requires an independent trustee. As an optional feature, an APT may also name a Distribution Director whose duties include directing the Independent Trustee to make distributions from the trust. A wealth owner can use this combination of features to create a governance structure for the trust that will facilitate sound financial decision-making even if the wealth owner’s mental capacity is diminished.

In some states, if the settlor of a trust includes a Statement of Purpose in the trust document, the rest of the trust must be interpreted with that statement in mind. For example, the Statement of Purpose can include a discussion of the settlor’s desire to assure sound financial management of the settlor’s assets after the settlor reaches a specified age.

Most importantly, when the APT is established, the wealth owner must have sufficient foresight to select an age at which the wealth owner will surrender any powers to remove and replace the Independent Trustee or Distribution Director. Thereafter, the power to remove and replace people serving in those roles should be held by a much younger person trusted by the wealth owner. The decision to include this feature is likely to prove critical in determining how successful the APT will be in protecting a portion of the family’s wealth from poor decision-making as the wealth owner’s mental capacity diminishes.

Conclusion

If you wish to protect yourself from your future self, you should seriously consider a structure such as a self-settled asset protection trust which contains features designed to compensate for your own loss of mental capacity. You may find this difficult because it is not easy to contemplate one’s own decline, and it is also not easy to give up control over financial decisions. The problem is particularly acute for those who have no healthy spouse who can step in to take control if necessary. The best solution for those situations is probably to name a trusted family member or attorney as the decision-maker.

This report is the confidential work product of Ballentine Partners. Unauthorized distribution of this material is strictly prohibited. The information in this report is deemed to be reliable but has not been independently verified. Some of the conclusions in this report are intended to be generalizations. The specific circumstances of an individual’s situation may require advice that is different from that reflected in this report. Furthermore, the advice reflected in this report is based on our opinion, and our opinion may change as new information becomes available. Nothing in this presentation should be construed as an offer to sell or a solicitation of an offer to buy any securities. You should read the prospectus or offering memo before making any investment. You are solely responsible for any decision to invest in a private offering. The investment recommendations contained in this document may not prove to be profitable, and the actual performance of any investment may not be as favorable as the expectations that are expressed in this document. There is no guarantee that the past performance of any investment will continue in the future.