Cautious Optimism Meets New Risks

The first quarter of 2026 began with a highly constructive backdrop that, at the time, appeared capable of extending the economic expansion and supporting financial markets. On February 28, however, that narrative materially changed course with the U.S. bombing of Iran. What followed was a notable shift in expectations—from a benign outlook to a more uncertain one shaped by geopolitical risk, rising inflation pressures, and a renewed conversation around recession risk. While our base case remains cautiously optimistic, we are a bit more cautious and a bit less optimistic than we were thirty days ago.

2026’s Strong Starting Point: The Policy Trifecta

At the outset of the year, the U.S. economy was benefiting from a rare policy “trifecta”. Fiscal policy, monetary policy, and credit policy were all aligned in stimulative mode. On the fiscal front, OBBBA provided a bevy of tax perks, including permanently lower income tax rates, expanded standard deductions, and targeted relief measures on overtime pay, tips, and Social Security income for certain retirees. Expanded SALT deductions and interest deductibility on car loans further supported the cause. Seemingly arcane accounting adjustments to how R&D is expensed created all sorts of incentives for companies to invest. And regulatory relief in the banking sector encouraged capital formation and credit extension.

Monetary policy was equally supportive. The Federal Reserve had implemented seven rate cuts totaling 1.75% prior to the start of the year, and markets were anticipating further easing. Given that rate cuts have a lagged effect, 2026 was going to be the true beneficiary of all of this cheaper money.

At the same time, credit conditions were highly accommodative. Banks were willing lenders, and borrowing costs were a bargain, with credit spreads at 27-year lows. It sounds ridiculous, but Microsoft was borrowing money at a cheaper rate than the Federal government! This was a clear indication of abundant liquidity and strong investor demand for credit.

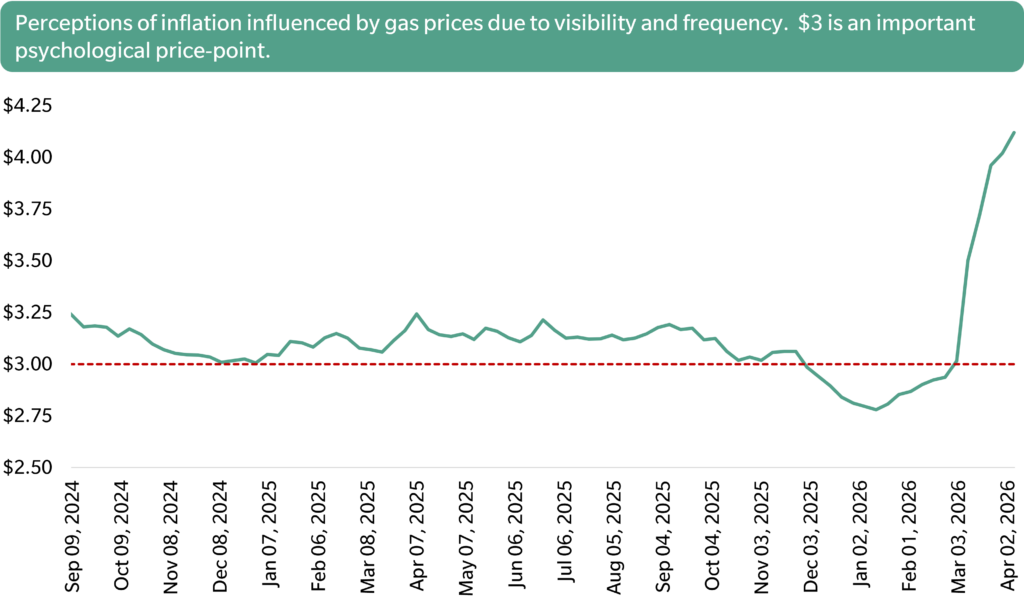

Profit margins for the S&P 500 reached all-time highs, mirrored by similar strength in developed international markets. The consumer, which remains the backbone of the U.S. economy, appeared resilient. Real wages had been rising for 34 straight months, unemployment remained near multi-decade lows, and discretionary spending indicators—from air travel to entertainment—were strong. Inflation expectations, which had been a persistent concern in prior years, were beginning to moderate. Gasoline prices had dropped to $2.76 nationwide by the end of February. In short, the economic and market environment entering 2026 was solid. While not without risks, the prevailing view was that the expansion had further room to run.

A Sudden Shock

That outlook changed abruptly on February 28, the day the U.S. started bombing Iran and continued relentlessly throughout the month of March. Oil prices, which had remained below $70 per barrel for much of 2025, surged to over $120 within weeks. Gasoline prices rose 49%, breaching $4 per gallon, a dramatic reversal with both economic and psychological implications.

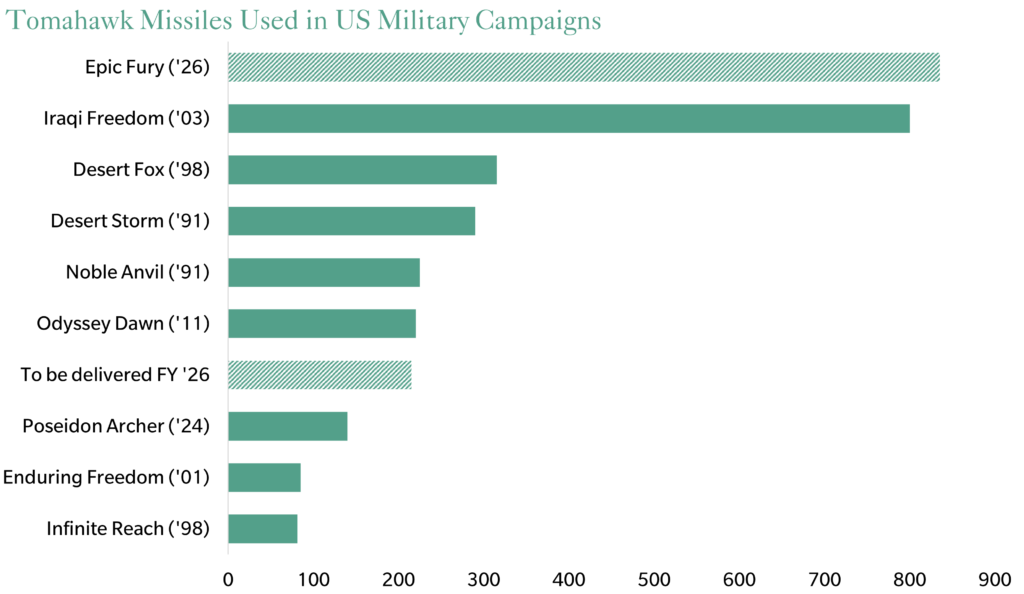

U.S bombing activity in Iran has been profound

Source: Center for Strategic and International Studies (CSIS)

Gasoline prices over the last 18 months

Source: U.S. Energy Information Administration

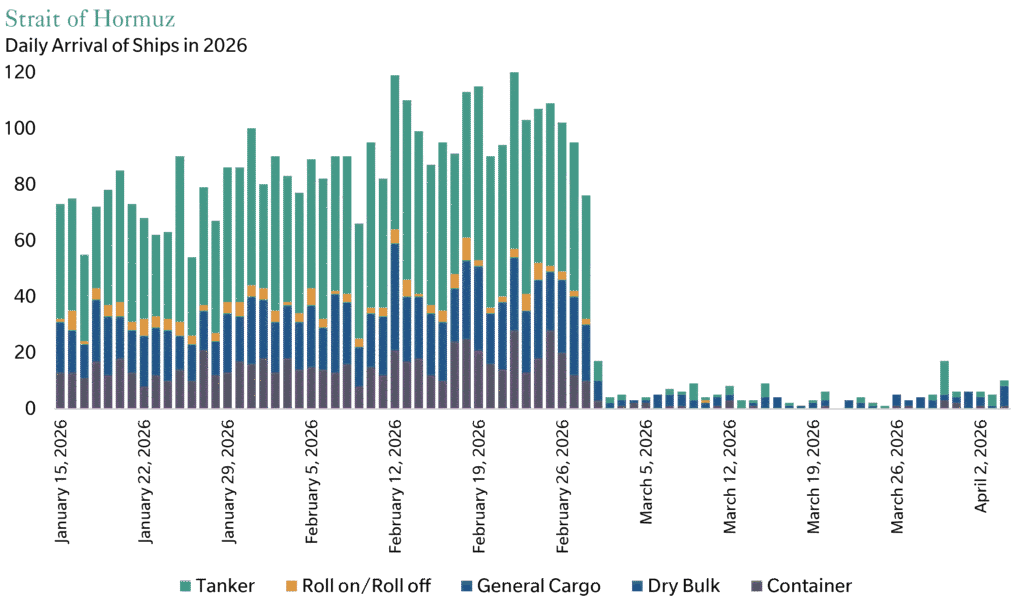

This was not simply a gasoline story. The Strait of Hormuz, now referred to as the “choke point,” is central to the movement of a myriad of industrial inputs. Liquified natural gas is a key ingredient in fertilizer production, so supply disruptions raised concerns about agricultural output and food prices. Petrochemical shortages affected manufacturing sectors reliant on plastics and synthetic materials. Even niche but critical inputs, such as helium used in semiconductor production and medical equipment, faced constraints, highlighting the interconnected nature of modern supply chains.

Massive disruptions to oil shipments and other materials

Source: IMF Portwatch

Transportation costs rose as insurers priced in higher risks. Oil tankers and all manner of freight capacity tightened. Alternative shipping routes extended delivery times and increased fuel, labor, financing, and logistics costs. These dynamics introduced new inflationary pressures at a time when the global economy had only recently begun to stabilize.

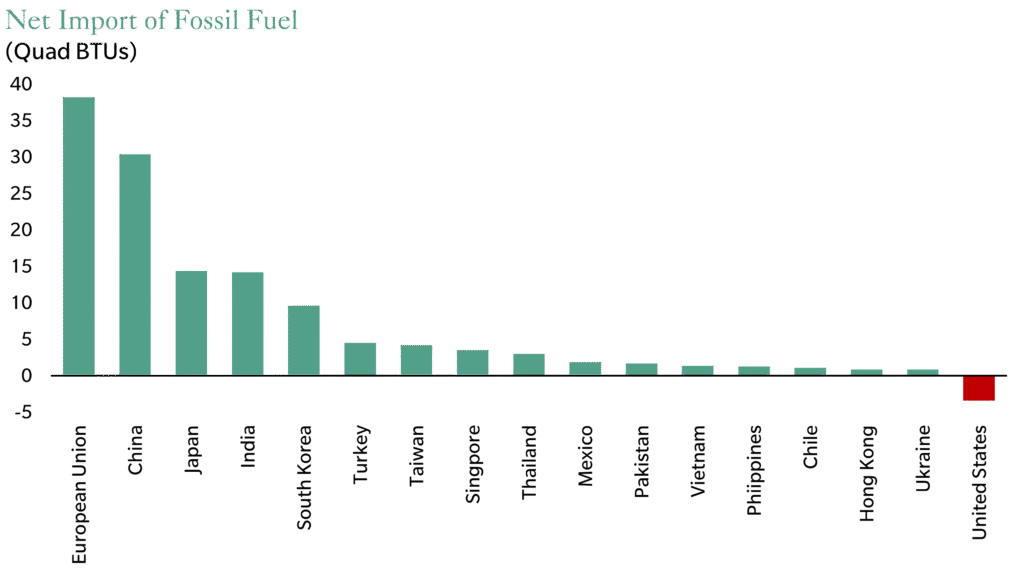

Expectations for additional Federal Reserve rate cuts evaporated. As inflation risks re-emerged, the prospect of further monetary easing diminished, removing a key pillar of support and hope for asset prices. Financial markets responded with a repricing of risk, though not uniformly. U.S. equities experienced a 5% pullback, while international and emerging markets—more dependent on imported energy, as the chart below shows—experienced sharp10% corrections.

U.S. is a net exporter of fossil fuel, unlike many large economies

Source: Goldman Sachs. Quad BTUs (quadrillion British thermal units) are a common energy unit. They convert coal, crude oil, refined products, natural gas (including LNG), and other fossil fuels into a single comparable measure based on heat content.

A Shift in Narrative

The cumulative effect of these developments has been a meaningful shift in the economic narrative. Where the year began with a focus on growth and policy support, the conversation has turned toward uncertainty and downside risks. Economists have begun to raise the probability of a recession, driven largely by the potential for sustained energy price increases and the secondary effects of supply chain disruptions.

It is important, however, to distinguish between heightened risk and a base case outcome. At present, we do not view a recession as the most likely scenario. The underlying economy entered this period of volatility from a position of strength. Household balance sheets remain relatively healthy, corporate profitability is still elevated, and the labor market, while showing some signs of normalization, is far from weak.

That said, the margin for error has narrowed. Elevated oil prices act as a tax on consumers and businesses alike. They reduce disposable income, increase operating costs, and can dampen both consumption and investment. If sustained, these pressures can slow economic growth meaningfully.

At the same time, central banks face a more complex policy environment. The resurgence of inflationary pressures limits their ability to provide additional stimulus. In fact, if inflation expectations become unanchored, policymakers may be forced to maintain or even tighten financial conditions, something unthinkable just a month ago.

The Role of Policy and Politics

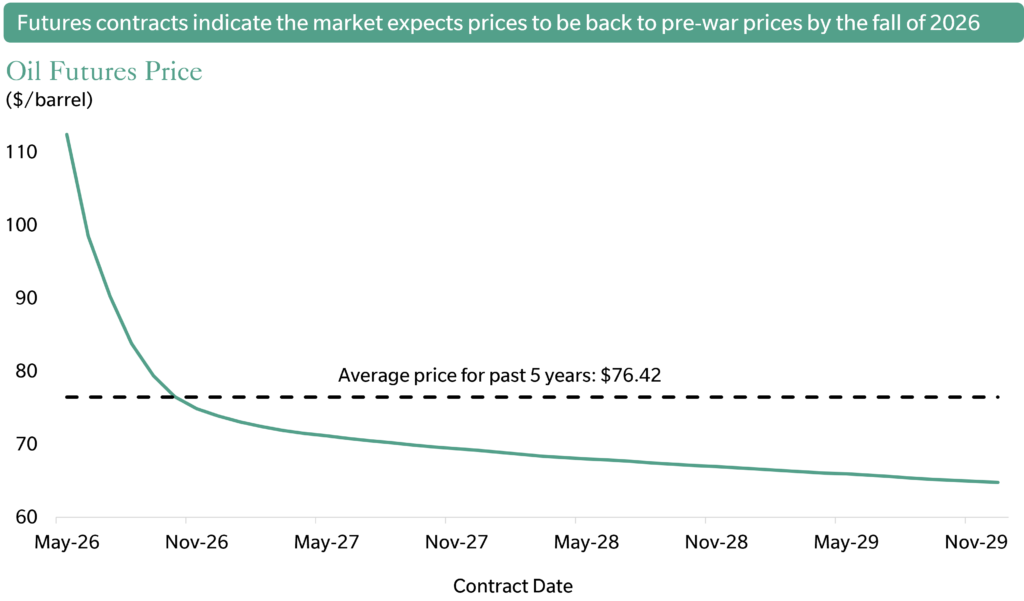

Overlaying these economic dynamics is a rapidly evolving political landscape. Extraordinarily provocative threats from the Trump administration have many on high alert. As we write this note, Iran and the U.S. have just negotiated a two-week ceasefire and oil prices declined 15% overnight. But the situation remains fraught. It is proper to note that the administration faces significant pressure to resolve the war quickly. Rising energy prices are political minefields, particularly in the context of the upcoming November midterm elections. There is a strong incentive to find a resolution—political analysts call it Trump’s “exit-ramp.” Energy futures pricing suggests an expectation that tensions will ease in the coming months, allowing oil prices to normalize by the fall.

Oil price increases expected to be temporary

Source: CME Group as of April 7, 2026. WTI Oil

However, this expectation is not without risk. Geopolitical events are inherently unpredictable, and the range of potential outcomes remains wide. This is not a time for bold predictions and confident “bets.” Just the opposite. This is a time of maximum uncertainty. And maximum humility.

Investment Implications

For investment portfolios, this environment requires a careful balance between discipline and flexibility. Periods of heightened uncertainty often lead to increased market volatility and uneven performance across asset classes and regions. The dispersion we have already observed—between U.S. and international equities, for example—may persist as markets continue to adjust to evolving conditions.

It is also worth noting that markets tend to move ahead of the underlying economy. Much of the recent repricing reflects expectations about future conditions rather than current realities. As such, periods of dislocation can create both risks and opportunities. Modestly good news could trigger an outsized rally when bad news is already priced in.

Maintaining a diversified portfolio remains critical. Exposure to a range of asset classes and geographies can help mitigate the impact of localized shocks. At the same time, a focus on quality—both in terms of corporate balance sheets and earnings durability—becomes increasingly important in uncertain environments.

Our Perspective

The key takeaway from the first quarter is not that the economic outlook has turned negative but that it has become more complex and uncertain. We are a bit more cautious and a bit less optimistic than we were thirty days ago.

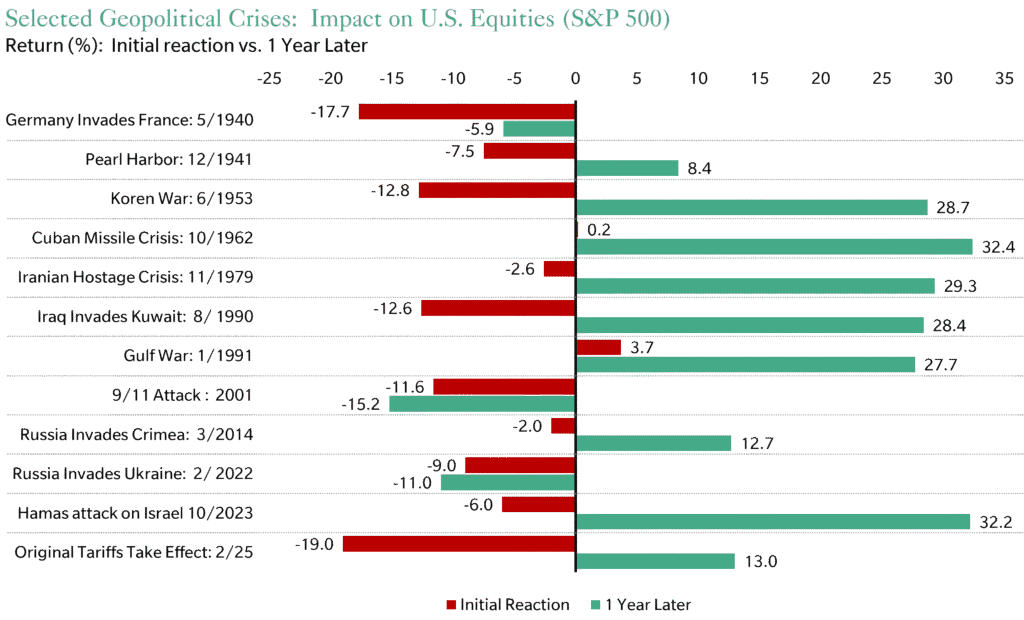

We are operating in an environment where minute-by-minute developments can have outsized effects on markets and sentiment. This makes it tempting to react to headlines or attempt to anticipate near-term outcomes. History suggests that such approaches are rarely successful. Quite the opposite, actually. History suggests that staying the course is typically the best strategy, as markets come out of the uncertainty tunnel better than when they entered. See chart below, which highlights a string of historical crises, many related to the Middle East. The short-term reaction, no surprise, is typically negative; within a year, however, markets have, more often than not, recovered early losses and then surpassed them.

Crises and Equities: Bad immediately, but typically benign a year later

Source: Ballentine Partners and NDR. Past performance is not necessarily indicative of future performance.

Also, we remain focused on longer-term fundamentals. The global economy has demonstrated resilience in the face of numerous challenges over the past several years. While the current situation introduces new risks, it does not, in our view, fundamentally alter the trajectory of long-term growth. AI investments remain robust. Earnings growth remains rock solid. Profit margins continue to improve. The consumer, despite feeling pinched by higher prices, is actually still experiencing wage growth above and beyond inflation. Our recent shift of assets into international stocks may actually be helped in the long-term by a strategic fiscal response (i.e, infrastructure buildout) by the likes of Germany, in particular, as they and the rest of Europe continue to diversify their oil and natural gas sourcing. Energy resilience and energy independence are not new buzzwords, but there is a new urgency to them.

No matter, short-term volatility will remain elevated, and the range of potential outcomes is wider than it was just a month ago. Those potential outcomes could have even changed by the time you are reading this. This calls for a measured approach, one that acknowledges uncertainty without overreacting to it.

Conclusion

The first quarter of 2026 serves as a reminder of how quickly the economic and market landscape can change. The year began with strong tailwinds. Yet seemingly overnight, it shifted to uncertainty and chatter about a rising risk of recession.

As always, our focus is on navigating these conditions with a disciplined, long-term perspective. The economy is still growing. People have jobs. Wages are rising. Consumption appears steady. We will continue to monitor the Iran situation and its secondary and tertiary downstream effects closely but without losing sight of the principles that guide our investment approach.

The past decade has seen numerous and painful double-digit stock market corrections that triggered sleepless nights, angst, or agita. Or all three. Yet time after time, resilience, diversification, discipline, rebalancing, loss-harvesting, and cool heads saw us through the fog. We will continue this approach and these strategies in order to focus on our long-term perspective.

About Pete Chiappinelli, CFA, CAIA, Chief Investment Officer

Pete is a Partner and Chief Investment Officer at the firm. He is focused primarily on Asset Allocation in setting strategic direction for client portfolios.

This report is the confidential work product of Ballentine Partners. Unauthorized distribution of this material is strictly prohibited. Information obtained from third-party sources is believed to be reliable; however, the accuracy of the data is not guaranteed and may not have been independently verified. Some of the conclusions in this report are intended to be generalizations. The specific circumstances of an individual’s situation may require advice that is different from that reflected in this report. Furthermore, the advice reflected in this report is based on our opinion, and our opinion may change as new information becomes available. Nothing in this presentation should be construed as an offer to sell or a solicitation of an offer to buy any securities. You should read the prospectus or offering memo before making any investment. You are solely responsible for any decision to invest in a private offering. The investment recommendations contained in this document may not prove to be profitable, and the actual performance of any investment may not be as favorable as the expectations that are expressed in this document. There is no guarantee that the past performance of any investment will continue in the future.